STRONG PARTNERSHIPS REQUIRED

The EU and ASEAN Joint Working Group on Palm Oil recently defined an ambitious agenda of research, dialogue and cooperation. That is excellent news, because EU legislation is dead on arrival without strong partnerships. There are a lot of issues to be discussed around finding common ground to foster an energetic partnership.

Let’s explore some critical issues on the agenda as we move away from disinformation, boycott strategies, and anti-palm oil marketing. In brief, I will first evaluate the old debate on biofuel and explore the new dialogue on legislation. Finally, I will share some thoughts on refocusing on the pressing issues of deforestation through an economic lens.

Let’s move away from disinformation, boycotts, and anti-palm oil marketing.

BIOFUEL: ENDING THE WAR

For many years the ASEAN-EU dialogue on palm oil was dominated by a polarized debate on the use of palm oil for biofuel. The European Commission ended the debate unilaterally in March 2019 by announcing it would phase out palm oil in biodiesel by 2030. This policy did not take into account the differences in productivity and carbon emissions between palm oil and vegetable oil alternatives from European sources. That verified scientific data is significantly in favor of palm oil.

At the same time, recent market intelligence clearly shows that transport’s transition to electric power is gaining momentum. The diesel engine will be obsolete by the end of the decade, regardless of the outcome of ongoing WTO procedures that are still dealing with conflicts that have lost their meaning given the status of the energy transition.

Not only is the noisy and dirty combustion engine fast becoming a technology of the past, it is inextricably linked to the software tampering scandal corrupting the integrity of EU regulations. Still, the fact that there is no future for biodiesel in Europe is not because of EU parliament resolutions, but because of the changing realities of the renewable energy transition. A similar process can be observed in countries like China and India, which are rapidly moving towards electric cars.

It is high time to bury the hatchet.

MANDATORY DUE DILIGENCE IS THE NEW ROUTE

The European market is already moving from voluntary standards to legislation, defining and enforcing sustainability by law. This process is being accelerated by the global climate ambitions that translated the Paris Climate Agreement into the European Green Deal, aiming to make the EU climate neutral by 2050. The Farm to Fork strategy at the heart of the Green Deal seeks to make food systems fair, healthy, and environmentally friendly. This strategy combines both regulatory and voluntary initiatives, using the synergy between good governance and market-driven commitments.

EU Market figures

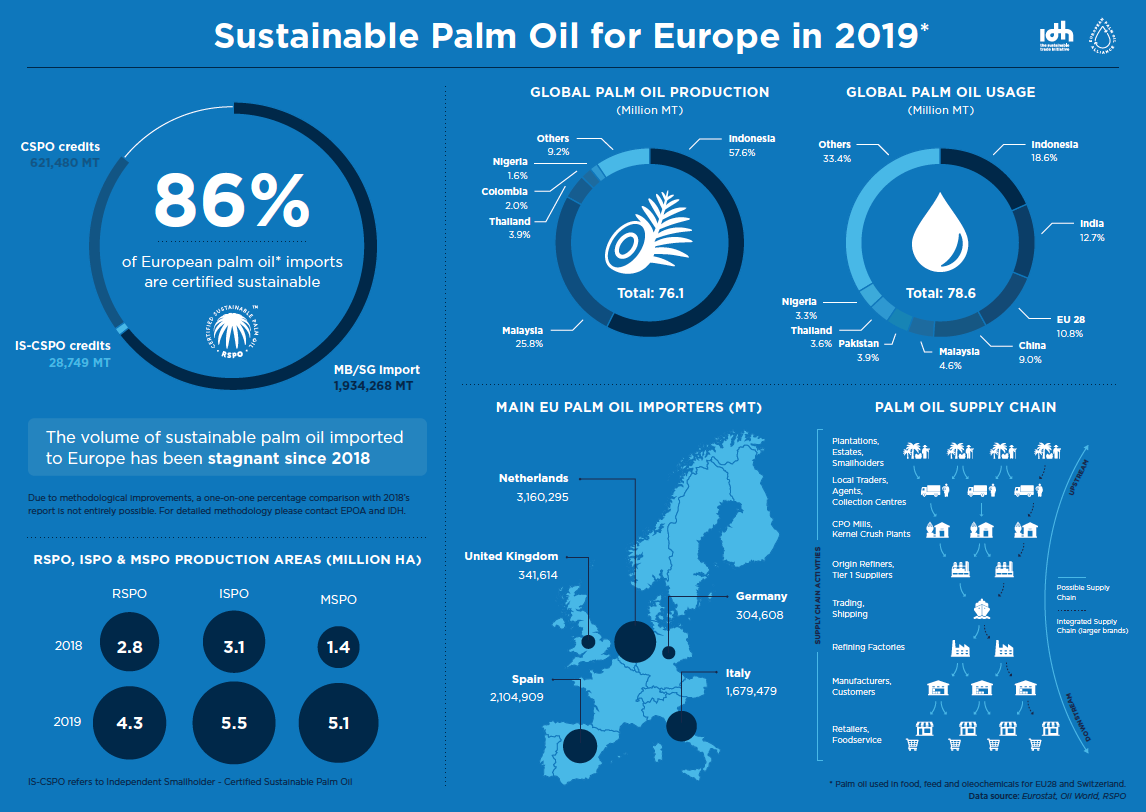

Recent figures show that Europe is a de facto RSPO dominated market: More than 86% of palm oil imports are already RSPO-certified.

BEYOND THE EU

Asian palm oil exporters’ voluntary sustainable certification under the RSPO scheme is no longer seen as a market barrier or distortion. More than enough certified palm oil volumes can be shipped to the EU to meet demand. New mandatory sustainability requirements are not an issue for exporters, partly because sustainable volumes receive a market price premium as an incentive. There is more hesitation in political circles. The EU’s failure to recognise the importance of the national sustainability standards in Malaysia and Indonesia (the MSPO and ISPO respectively) is a serious worry for governments.

But there is a further consideration. The EU’s ambition must go beyond cleaning its own footprint of palm oil imports. Europe only represents 6.4% of the global palm oil market. Making this relatively small volume sustainable will not bring systemic change –including upscalable innovative solutions and structural benefits for farmers – to the sector as a whole.

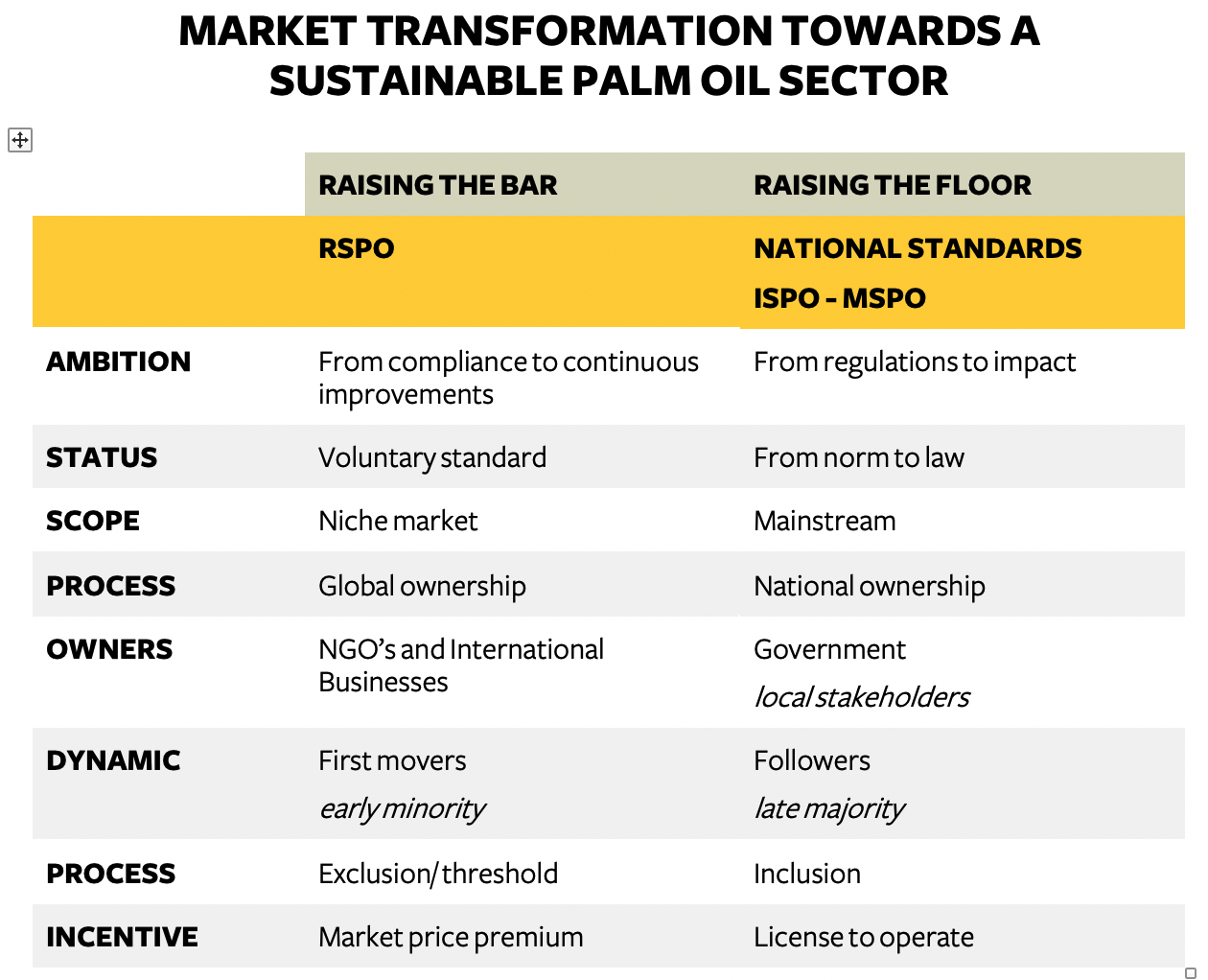

NATIONAL STANDARDS VERSUS VOLUNTARY STANDARDS

Right now, there is an opportunity to reconcile positions and strengthen cooperation worldwide. Politicians are likely to agree that at the end of the day, only governments have the mandate, authority, and responsibility to transform national agricultural and industrial sectors to ensure they meet ambitious sustainability standards in line with international agreements. That’s why national standards are the vehicle of choice for sector transformation that leaves no-one behind, raising the floor through legally binding minimum requirements. These should work side by side with voluntary standards as a way for first movers to raise the bar, continuously testing further improvements. In this optimal dynamic of interactions, the power of markets and of good governance are constructively combined.

National standards are the preferred vehicle for sector transformation.

The moment has come to fully acknowledge the relevance of the national sustainability standards for the palm oil transition in Indonesia and Malaysia. The creation of a EuropeAid-funded producer support programme for implementation and improvement of ISPO and MSPO, with a focus on smallholder inclusion, will open a new chapter beyond polarisation. Bringing legislation to life requires collective action.

Mandatory regulations and voluntary standards are both needed for optimal outcomes.

DOES PALM OIL REALLY DRIVE DEFORESTATION?

Deforestation is a very critical subject in the building of a more common understanding. In the dominant discourse in the West, the expansion of the palm oil sector is identified as the main driver of large-scale deforestation: it is blamed for the destruction of one of the last remaining rainforest biomes, situated in the Southeast Asian archipelagos. It is crucial to look beyond this facile conclusion to create effective, scalable solutions that tackle the issue’s root causes.

The real driver of palm oil-related deforestation is poverty – on the production side, palm oil appears to offer improved prospects to millions of farmers, while on the market side, there is strong demand from low-income consumers for affordable cooking oil. These combined economic forces have driven the growth of the palm oil sector as an economically efficient solution for decades. Forests are hard to maintain unless trees are worth more standing than cleared. Otherwise, there is always some crop or other that is seen as a good reason to cut them down. Alternatives like cocoa, coffee, tea, rubber, timber, or rice are less productive and will accelerate the expansion of agriculture at the cost of forest even faster. Millions of smallholder farmers will be negatively impacted. Competing land use against forest requires an economic response; making maintaining forests an economically valuable alternative. No palm oil substitute can solve this challenge. In reality there will be even an opposite effect. Forests are hard to maintain unless trees are worth more standing than cut down.

HOW TO OFFSET THE OPPORTUNITY COSTS

The core question is this: Can we build effective financial mechanisms to offset the opportunity costs of keeping the forest standing? These costs should not just be borne locally. Given the discrepancies in forest coverage between continents and their stages of development, an international settlement is needed. Asian-European cooperation must include this financial dimension, possibly as part of the proposed EuropeAid funding.

Investment in maintaining the forest should be shared by all actors in the supply chain.

MARKET-BASED SOLUTIONS

In essence there are two parallel routes to take: Market-based solutions and good governance. Combining the two is most probably the smartest way forward. Market-driven solutions to deforestation entail developing the farmer business case for sustainable palm oil production in at least two scenarios:

- One is the concept of agroforestry, combining agriculture with forest coverage and using the economic potential of intercropping without destroying biodiversity. Most probably, this scenario will require additional earnings for farmers to achieve a living income. These could take the form of payments for environmental services and carbon sequestration. As mentioned before, the resulting financial burden cannot be borne locally; all supply chain actors must contribute.

- Secondly, agroecology could redefine the concept of palm oil cultivation at scale, moving from maximization to optimization of production while respecting the boundaries of the landscape and ecosystems. This would help preserve fertile soils, clean water, biodiversity, carbon storage, and other environmental services on which we are all heavily dependent. Markets are best positioned to bring together the innovative power of science and technology, capital, and entrepreneurship to accelerate these innovations towards functioning agroecological systems.

GOOD GOVERNANCE: ANOTHER CRUCIAL COMPONENT

The existence of public goods and the provision of ecosystem services like clean air, water, fertile soils, and biodiversity,should not depend on their economic value alone. Society – as represented by governments – has a responsibility to safeguard these for future generations. This requires a very different timeline than short-term profits. If we put a monetary value on public goods as a strategy to save it, there is a risk of its being appropriated by the wealthy few. Governance on a global scale is required to deal with climate change and other cross-border issues like poverty, migration, fair trade relations, epidemics, etc. The Green Deal is a laudable European interpretation of a continental responsibility to deliver sustainable development solutions. At the same time, we are all interconnected with other continents through trade relations. One-sided measures will not have a positive outcome. Financial transfers to help developing countries are crucial to achieve outcomes that serve the worldwide community as a whole.

The EU and ASEAN Joint Working Group on palm oil is to meet again, preceded by expert meetings, to discuss possible two-way cooperation. Let’s put the conflict behind us and work together.

Nico Roozen

*This article originally appeared on LinkedIn.